Investors who spend time around the energy sector quickly notice that not every opportunity comes through public markets. While many people gain exposure through stocks, funds, or large integrated companies, others are drawn to structures that offer a more direct connection to production activity. These opportunities can be appealing because they feel tangible and closely tied to the underlying asset. Instead of simply owning shares in a corporation, investors may participate in projects that depend on drilling results, operating performance, and the commercial strength of producing wells.

That direct connection can create both excitement and responsibility. Energy projects are influenced by geology, engineering, commodity prices, infrastructure, and the quality of operational decision-making. A well-structured project with experienced leadership may offer meaningful upside, but the same sector can punish investors who rely too heavily on optimistic forecasts or incomplete due diligence. For that reason, direct participation in oil and gas is usually best approached with a careful review of documents, a realistic view of costs, and a strong understanding of how revenues and obligations are shared.

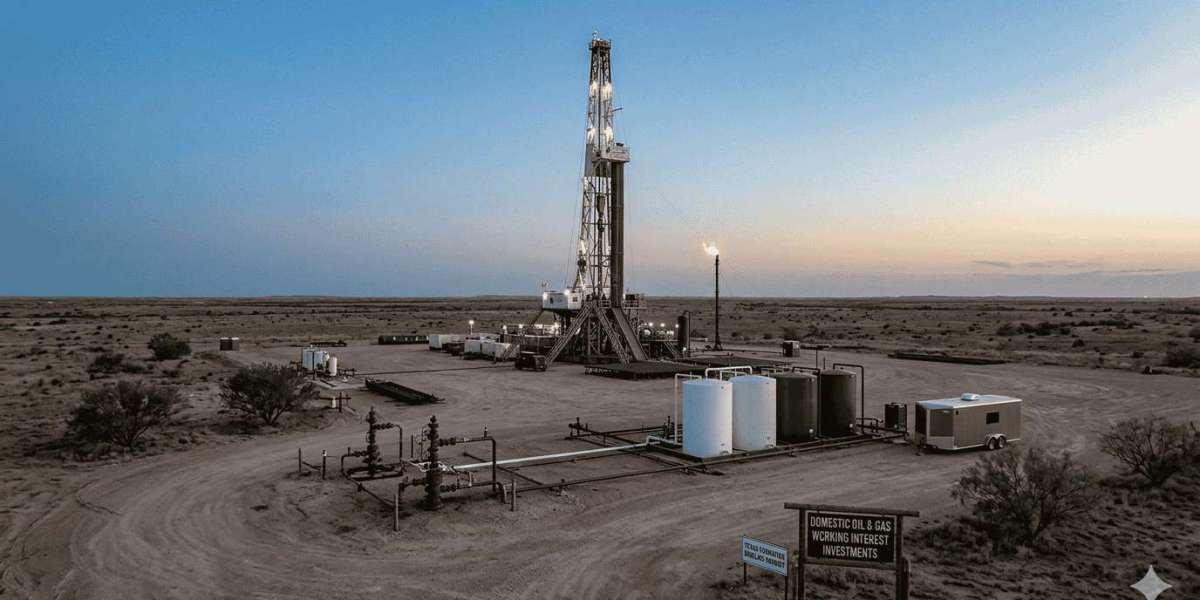

One structure that often attracts attention is Oil and Gas Working Interest Investments. These arrangements are appealing to some investors because they can provide direct participation in the economics of a producing asset rather than indirect market exposure alone. In the right setting, they may offer the possibility of revenue tied to production, participation in domestic development, and a closer relationship to the performance of the underlying wells. At the same time, this type of investment is not passive in the way many public securities are. Investors need to understand that returns can be affected by operating expenses, project timing, production variability, and commodity price swings.

A disciplined investor will therefore focus on more than projected upside. It is important to ask whether the operator has a proven history in the basin, whether the geological assumptions are supported by nearby data, and whether the economics still work if prices move lower than expected. Strong presentations can make any energy project look attractive, but the real test is how the opportunity performs under pressure. Capital costs, completion methods, lease terms, decline curves, and transportation access can all influence final results. These details are not secondary. They are central to whether the project can create value over time.

Another important consideration is portfolio fit. Direct energy participation can be more concentrated and less liquid than traditional investments, which means it should be evaluated in the context of the investor’s broader financial picture. Some individuals may be comfortable with commodity-linked risk and long-term project horizons, while others may prefer more diversified or publicly traded forms of exposure. Knowing the difference can help prevent a mismatch between expectations and reality.

Energy has always rewarded those who combine interest with discipline. Direct participation may offer a compelling path for investors who want deeper involvement in the sector, but it works best when decisions are guided by data, operator quality, and realistic assumptions rather than enthusiasm alone.