Market Overview and Growth Outlook

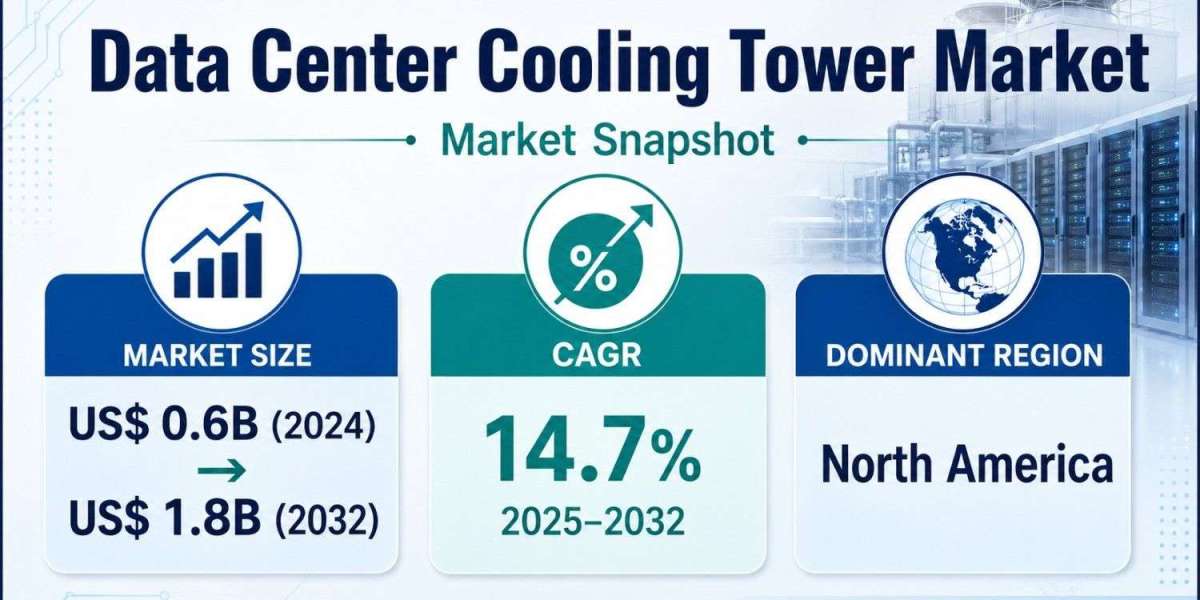

The Data Center Cooling Tower Market forecast indicates sustained expansion through 2032. Market value is expected to increase from US$ 0.6 billion in 2024 to US$ 1.8 billion by 2032 as operators invest in systems capable of rejecting heat from larger and more demanding computing environments.

“The Data Center Cooling Tower Market is expected to grow at a CAGR of 14.7% during 2025–2032.” Increased server density, cloud adoption, AI processing, and high-performance computing are raising heat loads and strengthening the operational need for dependable thermal infrastructure.

Cooling towers help maintain optimal equipment temperatures by transferring heat from water-cooled systems to the atmosphere. The Data Center Cooling Tower Market forecast reflects their role in supporting chiller efficiency, uptime, and scalable data center development.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/data-center-cooling-tower-market#form

Market Segmentation Analysis

By Data Center Type, the market is segmented into Hyperscale, Colocation, Enterprise, and Edge. Colocation leads because shared infrastructure gives enterprises a scalable and cost-efficient alternative to owning and operating dedicated capacity. This outsourcing model generates continuing requirements for robust cooling equipment.

Colocation sites must support multiple customer workloads at high utilization. Their cooling systems need to respond to different rack densities and changing thermal patterns while meeting demanding service and uptime conditions. Centralized and redundant cooling is consequently a core operational requirement.

Hyperscale data centers are the fastest-growing category. Their growth is connected to cloud-provider investment and the expansion of AI and data-intensive processing. Cooling towers support the resulting high thermal loads through scalable water-cooled architectures designed for large facilities.

By Product Type, the market is segmented into Natural and Mechanical [Counter Flow Configuration and Cross Flow Configuration]. Natural towers maintain the largest market share because they can handle high cooling loads through natural airflow, reducing energy consumption at scale. Large campuses with sufficient land are particularly suited to this design.

Mechanical cooling towers record faster growth because of their compact format, controllability, and deployment flexibility. They can be integrated into urban, modular, and space-constrained facilities where precise temperature control and adaptable configurations are important operating considerations.

By Tower System Type, the market is segmented into Wet and Dry. Wet systems continue to dominate based on proven reliability and efficient heat rejection. Their ability to perform consistently under varying and continuous loads supports adoption across critical data center environments.

Dry systems are seeing selective adoption where operators seek to minimize water consumption. Their relevance increases in water-scarce locations and regions with restrictive environmental conditions. Broader growth remains moderated by higher capital costs and lower thermal efficiency relative to wet systems.

Regional Market Insights

North America holds the leading market position. A dense base of hyperscale and colocation facilities, established digital infrastructure, and early use of advanced energy-efficient cooling technologies support regional demand. Investment in both new facilities and upgrades maintains requirements for high-capacity cooling towers.

Asia-Pacific is forecast to expand fastest. Rising cloud adoption and digitalization are encouraging data center construction across China, India, and Southeast Asia. Hyperscale and edge investments, supported by internet growth and enterprise demand, are increasing the requirement for scalable heat-rejection systems.

Emerging Trends Shaping the Data Center Cooling Tower Market

Operators are placing greater emphasis on cooling efficiency as electricity prices and sustainability commitments affect data center planning. Cooling towers can improve chiller performance and reduce total power consumption, contributing to lower Power Usage Effectiveness and more efficient facility operations.

Innovation is concentrating on hybrid tower designs, water optimization, and free cooling integration. These developments allow operators to address environmental considerations while preserving the thermal performance and reliability required for continuous data center workloads.

Liquid-cooling adoption is creating a complementary opportunity rather than eliminating cooling tower requirements. Direct-to-chip, immersion, and rear-door systems can connect to water-cooled or hybrid loops, which still require effective facility-level heat rejection.

Key Growth Drivers of the Market

- Digital infrastructure construction: New data center projects increase the number of facilities requiring cooling towers and related thermal equipment.

- Cloud capacity expansion: Cloud providers are building larger computing environments, creating demand for scalable and centralized cooling systems.

- Higher rack heat loads: Dense servers and advanced processors require efficient heat rejection to preserve uptime and equipment performance.

- Efficiency and PUE targets: Cooling towers can improve chiller performance and reduce energy consumption, supporting operational-efficiency goals.

- Environmental commitments: Carbon-reduction objectives and water-management requirements encourage investment in advanced, hybrid, and optimized cooling designs.

Competitive Landscape

Top Companies in the Market

- Baltimore Aircoil Company (BAC)

- Delta Cooling Towers, Inc.

- EBARA Corporation

- ENEXIO Management GmbH

- EVAPCO, Inc.

- Hamon Group / Hamon

- Johnson Controls International plc

- Kelvion Holdings GmbH

- Paharpur Cooling Towers Ltd.

- SPX Cooling Technologies

Conclusion and Strategic Outlook

The Data Center Cooling Tower Market is forecast to reach US$ 1.8 billion by 2032, advancing at a CAGR of 14.7% during 2025–2032. Demand is being shaped by cloud infrastructure, AI computing, data center construction, energy-efficiency priorities, and the use of cooling towers alongside liquid-cooling systems.

The strategic outlook centers on managing greater thermal intensity while controlling power use, water consumption, and operating costs. Cooling tower technologies that align performance with site-level constraints will remain important to the development of reliable digital infrastructure.

FAQs – Data Center Cooling Tower Market

1. What is the Data Center Cooling Tower Market forecast for 2032?

The Data Center Cooling Tower Market is forecast to reach US$ 1.8 billion by 2032. It was valued at US$ 0.6 billion in 2024.

2. What CAGR will the market register?

The market is expected to register a CAGR of 14.7% during 2025–2032. This represents strong growth across data center thermal-management infrastructure.

3. What is supporting the forecast?

The forecast is supported by expanding hyperscale and colocation capacity, cloud adoption, AI workloads, high-performance computing, and energy-efficiency requirements. New data center construction adds further demand.

4. Which regions are central to the forecast?

North America is the current market leader because of its established digital infrastructure. Asia-Pacific is the fastest-growing region as cloud services and data center investments expand.

5. What challenges may affect future investment?

Cooling choices are affected by water resources, electricity costs, environmental rules, capital requirements, and thermal-efficiency needs. These factors can influence whether wet, dry, natural, or mechanical systems are selected.