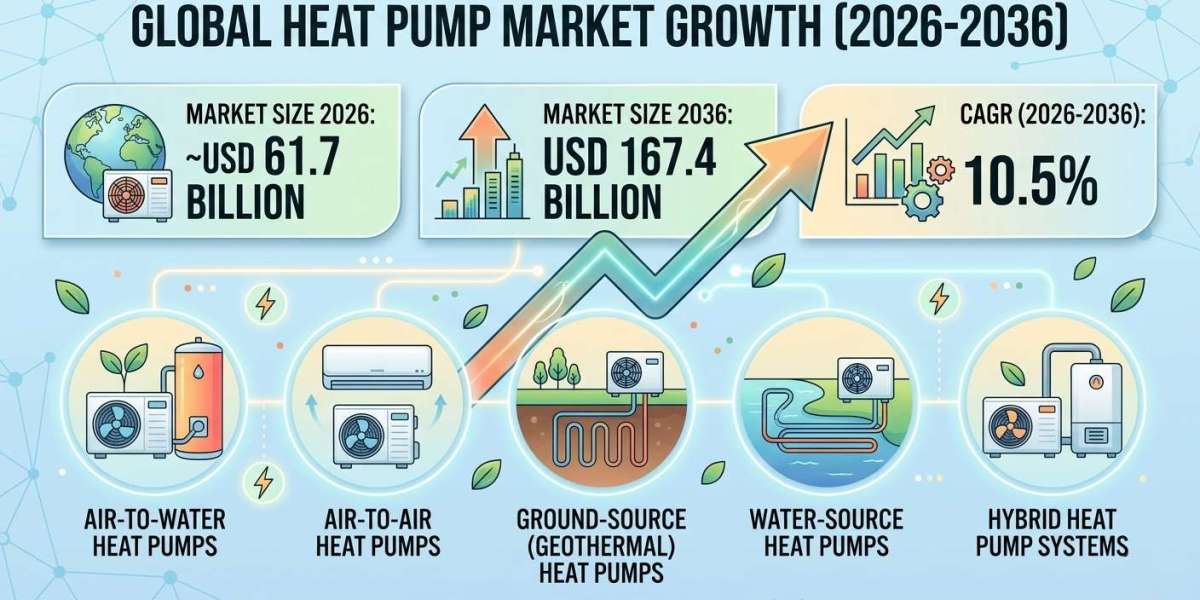

The global heat pump market is expected to witness strong expansion over the next decade, increasing from approximately USD 61.7 billion in 2026 to USD 167.4 billion by 2036, registering a CAGR of 10.5%, according to the latest analysis by Future Market Insights (FMI).

Market growth is primarily being driven by the global transition toward electrified heating systems, decarbonization policies, and rising energy-efficiency regulations across residential and commercial buildings. Governments and utilities across Europe, North America, and Asia Pacific are actively encouraging the replacement of fossil-fuel heating systems with energy-efficient heat pumps.

Heat Pump Market Snapshot (2026–2036)

Market size in 2026: USD 61.7 billion

Market size in 2036: USD 167.4 billion

CAGR (2026–2036): 10.5%

Leading technology segment: Air-to-Air Heat Pumps (~46.1% share)

Key growth regions: Europe, Asia Pacific, North America

Major end-use sector: Residential buildings

Momentum in the Market

Starting at approximately USD 61.7 billion in 2026, the heat pump market is projected to expand rapidly throughout the forecast period as countries accelerate electrification of building heating systems and pursue climate-neutral infrastructure targets.

By the early 2030s, market growth will be reinforced by rising retrofit demand, particularly in developed economies where aging heating infrastructure is being replaced with energy-efficient alternatives. Heat pumps are increasingly selected as the primary heating solution due to their ability to provide both heating and cooling through a single system.

Between 2030 and 2036, technological improvements such as inverter-driven compressors, enhanced heat exchangers, and advanced digital control systems will further improve system efficiency and performance reliability. Integration with renewable electricity sources and smart grid platforms is also strengthening the long-term value proposition of heat pump installations.

The Reasons Behind the Market’s Growth

Demand for heat pumps is rising as governments and building operators seek low-carbon heating technologies that align with climate targets and energy-efficiency mandates. Heat pumps operate by transferring heat from the surrounding air, water, or ground into buildings, making them significantly more efficient than conventional combustion-based systems.

Several factors are contributing to long-term market expansion:

Electrification policies aimed at reducing building emissions

Replacement of fossil-fuel heating systems with cleaner technologies

Government incentives and utility rebate programs supporting adoption

Lower operating costs compared with traditional heating equipment

Advancements in cold-climate heat pump technologies

Improvements in system design and refrigerant technologies are also helping manufacturers meet stricter environmental regulations, while maintaining heating capacity and year-round operational performance.

Top Segment: Technology Type

Air-to-Air Heat Pumps Lead with Around 46.1% Market Share

Air-to-air heat pumps represent the leading technology segment due to their ease of installation, cost efficiency, and widespread applicability in residential buildings. These systems are particularly popular in new construction projects and energy-efficient housing developments.

Other important heat pump technologies include:

Ground-source (geothermal) heat pumps, offering high efficiency for large installations

Water-source heat pumps, widely used in commercial and district heating systems

Hybrid heat pump systems, combining renewable heating with conventional systems for optimized performance.

Regional Development: Europe, Asia Pacific, and North America Lead Growth

The heat pump market is expanding rapidly across several global regions due to policy-driven decarbonization initiatives and growing demand for energy-efficient heating infrastructure.

Europe remains a leading market due to strong regulatory frameworks supporting electrified heating solutions and carbon reduction goals.

Asia Pacific is emerging as a key growth hub, supported by expanding urban construction and rising demand for sustainable HVAC technologies.

North America is witnessing strong adoption through federal and state-level energy-efficiency programs, along with increasing residential electrification initiatives.

Challenges, Trends, Opportunities, and Drivers

Drivers

Growing electrification of building heating systems

Government policies supporting low-carbon heating technologies

Rising demand for energy-efficient HVAC systems

Opportunities

Expansion of heat pump adoption in retrofit markets

Integration with renewable electricity and smart grid technologies

Growth in high-efficiency compressor and inverter technologies

Trends

Shift toward environmentally compliant refrigerants

Development of cold-climate heat pump technologies

Integration with smart home and building automation systems

Challenges

High upfront installation costs in certain regions

Infrastructure and installer availability constraints

Regulatory changes affecting refrigerant technologies

The Competitive Environment

The global heat pump market is highly competitive, with manufacturers focusing on energy-efficient product innovation, advanced compressor technologies, and environmentally compliant refrigerants.

Leading companies operating in the market include:

Daikin Industries Ltd.

Mitsubishi Electric Corporation

Carrier Global Corporation

Johnson Controls International

Viessmann Group

These companies compete through technology innovation, strategic partnerships, and expanded manufacturing capabilities to meet growing global demand for electrified heating solutions.

For a detailed strategic outlook and deeper analysis of technological developments shaping the industry through 2036, readers can explore the full report on the official Future Market Insights website:

https://www.futuremarketinsights.com/reports/heat-pumps-market