The global paper band market is transitioning from a niche packaging consumable into a compliance-aligned alternative to plastic bundling formats. As regulators tighten restrictions on single-use plastics and retailers push for recyclable, shelf-ready packaging, paper banding systems are gaining relevance across e-commerce, food, and consumer goods supply chains. What was once a low-cost bundling solution is now positioned at the intersection of sustainability mandates, automation compatibility, and brand presentation.

Quick Stats Snapshot

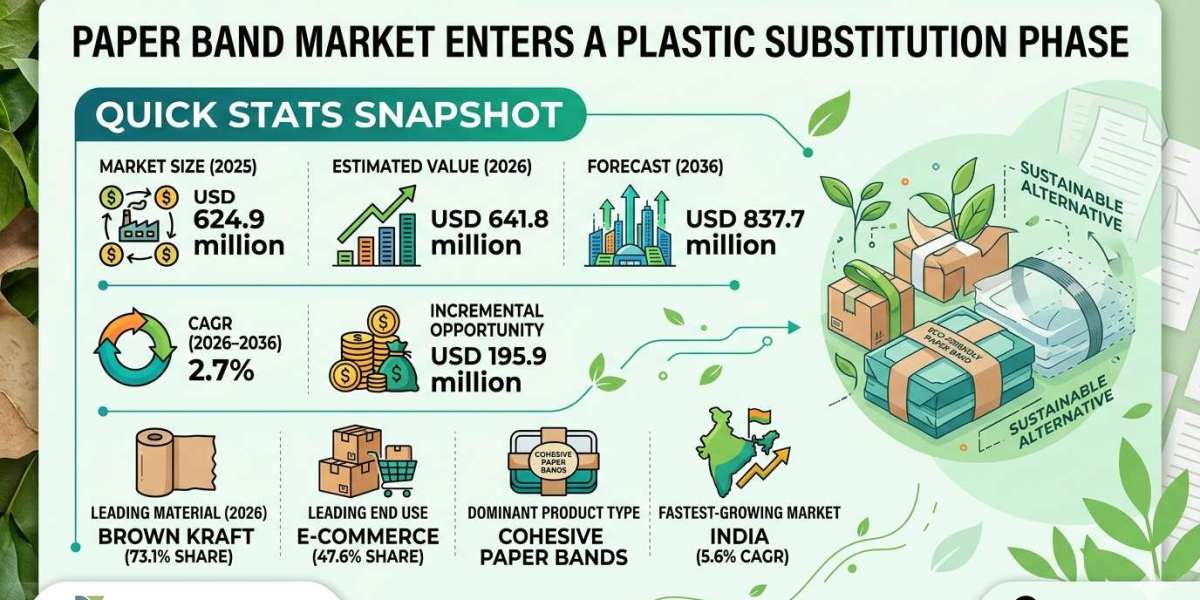

• Market Size (2025): USD 624.9 million

• Estimated Value (2026): USD 641.8 million

• Forecast (2036): USD 837.7 million

• CAGR (2026–2036): 2.7%

• Incremental Opportunity: USD 195.9 million

• Leading Material (2026): Brown Kraft (73.1% share)

• Leading End Use: E-commerce (47.6% share)

• Dominant Product Type: Cohesive Paper Bands

• Fastest-Growing Market: India (5.6% CAGR)

Market Size and Forecast

The paper band market is projected to expand from USD 641.8 million in 2026 to USD 837.7 million by 2036, reflecting a modest CAGR of 2.7%. Growth is steady rather than accelerated, shaped by gradual substitution of plastic strapping, shrink wrap, and polybags in selected applications.

Unlike high-growth packaging segments, paper banding remains a volume-driven consumables market, closely tied to e-commerce parcel flows, retail bundling formats, and food packaging applications. Demand expansion is less about new use cases and more about regulatory-driven material switching and operational compatibility with automated packaging lines.

Growth Drivers: Why Paper Banding Is Gaining Traction

1. Plastic Reduction Regulations

Government mandates across Europe and Asia-Pacific are accelerating the shift toward recyclable and mono-material packaging solutions, directly benefiting paper-based alternatives.

2. Expansion of E-Commerce Fulfillment

E-commerce accounts for 47.6% of demand, with paper bands widely used for bundling multipacks, securing parcels, and replacing plastic-based grouping materials.

3. Retail Shift Toward Shelf-Ready Packaging

Retailers are prioritizing packaging formats that enhance product visibility while reducing plastic usage, making paper bands an attractive option.

4. Compatibility with Automated Packaging Systems

Cohesive paper bands are increasingly integrated into high-speed packaging lines, improving efficiency while maintaining sustainability compliance.

Key Challenges: Cost, Material Volatility, and Performance Limits

• Raw Material Price Fluctuations: Variability in pulp and paper costs impacts production economics and pricing stability.

• Limited Load-Bearing Capacity: Paper bands are not suitable for heavy-duty bundling compared to plastic strapping.

• Moisture Sensitivity: Performance can be affected in humid or wet environments, limiting application scope.

• Low Differentiation: As a commoditized consumable, pricing pressure remains high across suppliers.

Emerging Opportunities: Where Market Value Is Evolving

Customization and Branding Integration

Paper bands are increasingly used as branding tools, enabling printed messaging, logos, and promotional content directly on packaging.

Food and Beverage Multipack Applications

Adoption is rising in bakery, fresh produce, and ready-to-eat segments where plastic-free packaging is becoming a requirement.

Automation-Driven Demand

Growth in automated fulfillment centers is increasing demand for cohesive bands that support high-speed operations.

Sustainable Packaging Portfolios

Brands are incorporating paper banding into broader sustainability strategies, replacing multiple plastic components with a single recyclable solution.

Segmentation Insights

By Material

• Brown Kraft (73.1%) dominates due to strength, durability, and compatibility with automated banding machinery.

• White Kraft is used selectively for branding and premium presentation.

By Product Type

• Cohesive paper bands lead due to suitability for automated systems and high-speed packaging lines.

• Preformed bands remain relevant for manual and semi-automated operations.

By End Use

• E-commerce (47.6%) is the largest segment, driven by parcel bundling and shipment preparation.

• Food & beverages represent a growing segment with increasing demand for plastic-free packaging.

• Personal care and pharmaceuticals use paper bands for labeling and secondary packaging.

Regional Analysis: Regulation and E-Commerce Shape Demand Patterns

Asia-Pacific: Growth Led by E-Commerce Expansion

• India (5.6% CAGR): Fastest-growing market, driven by rapid e-commerce adoption and organized retail expansion.

• China (4.3% CAGR): Growth supported by government restrictions on plastic packaging in delivery systems.

Europe: Regulation-Driven Adoption

France (1.9%) and Germany (1.0%) emphasize sustainable packaging due to extended producer responsibility (EPR) regulations and plastic reduction mandates.

North America: Mature but Stable Demand

The United States (1.4%) reflects steady demand across retail, food, and e-commerce sectors, with paper banding already established in specific applications.

Competitive Landscape: Differentiation Through Sustainability and Customization

The paper band market is moderately fragmented, with key players including Extra Packaging Corporation, SANDAR Industries Inc., Bandall, Cohesion Paper Products LLC, Graphic Arts Equipment, Brown & Pratt, Inc., American Printpack, and Economy Tablet & Paper.

Competitive advantage is defined by:

• Ability to offer recyclable and high-strength paper materials

• Integration with automated banding systems

• Custom printing and branding capabilities

• Cost efficiency and supply chain reliability

Innovation is focused less on material breakthroughs and more on operational efficiency, customization, and sustainability alignment.

Strategic Implications for Industry Stakeholders

• For E-Commerce Companies: Paper banding provides a scalable pathway to reduce plastic usage without disrupting fulfillment efficiency.

• For Retailers: Shelf-ready, branded paper bands enhance product presentation while meeting sustainability targets.

• For Packaging Suppliers: Differentiation depends on automation compatibility and customization capabilities rather than basic material supply.

• For Investors: The market offers stable, regulation-driven growth with limited volatility but constrained upside.

Future Outlook: Incremental Growth with Structural Relevance

The paper band market is not defined by rapid expansion but by its role in enabling incremental sustainability gains across packaging systems. As plastic reduction efforts intensify, paper banding will continue to replace specific use cases rather than dominate entire packaging categories.

Future growth will depend on improving material performance, expanding automation compatibility, and integrating branding functionality. While the market remains relatively small in value terms, its strategic importance within sustainable packaging ecosystems is expected to increase.

Executive-Level Takeaways

• The market is projected to reach USD 837.7 million by 2036, driven by plastic substitution trends.

• Growth remains modest at 2.7% CAGR, reflecting a mature, consumables-driven category.

• E-commerce is the dominant demand driver, accounting for nearly half of total usage.

• Brown kraft paper leads due to strength and cost efficiency.

• Regulatory pressure in Europe and Asia-Pacific is accelerating adoption.

• Customization and automation compatibility are emerging as key differentiators.

Full Report View: https://www.futuremarketinsights.com/reports/paper-band-market