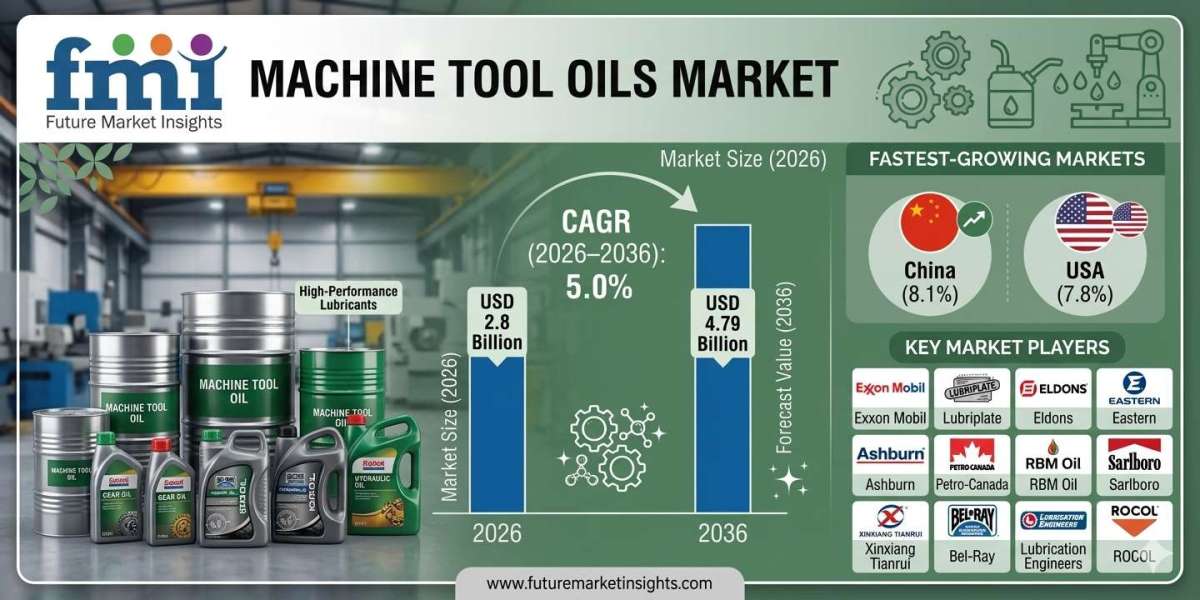

The global machine tool oils market is expected to witness stable and sustained expansion over the next decade, supported by rising industrial automation, increasing adoption of CNC machinery, and growing demand for high-performance lubrication systems across manufacturing industries. According to latest insights by Future Market Insights, the market is projected to grow from approximately USD 2.94 billion in 2026 to nearly USD 4.79 billion by 2036, registering a CAGR of 5.0% during the forecast period.

Market growth is being driven by the increasing utilization of machine tools in automotive, aerospace, heavy engineering, metal fabrication, and precision manufacturing operations. As industries continue modernizing production facilities and adopting advanced machining technologies, demand for reliable lubrication solutions capable of improving operational efficiency, minimizing wear, and extending equipment life is accelerating globally.

Machine tool oils are becoming increasingly critical for maintaining hydraulic systems, bearings, gears, slideways, and spindle operations in modern manufacturing environments. Manufacturers are also shifting toward synthetic and semi-synthetic oil formulations to comply with workplace safety standards, reduce maintenance cycles, and improve sustainability outcomes.

Machine Tool Oils Market Snapshot (2026–2036)

- Market size in 2026: USD 2.94 billion

- Forecast market value by 2036: USD 4.79 billion

- Forecast CAGR (2026–2036): 5.0%

- Leading product segment: Hydraulic oil (~45% market share)

- Leading application segment: Bearings (~20% share)

- Fastest-growing markets: China and India

- Primary demand driver: Precision manufacturing and industrial automation

Momentum in the Market

The machine tool oils market is entering a phase of technological transformation as manufacturers prioritize equipment reliability, energy efficiency, and longer operational life cycles. Between 2026 and 2036, increasing deployment of automated production lines and CNC-based machining systems is expected to create substantial demand for advanced lubrication products.

Industries are increasingly investing in high-speed machining equipment that operates under extreme thermal and pressure conditions, making premium lubrication systems essential for maintaining precision and reducing downtime. Machine tool oils are no longer viewed as basic maintenance consumables but as strategic operational assets that directly impact productivity and lifecycle costs.

Beyond 2030, the market is expected to benefit from the expansion of smart factories and Industry 4.0 manufacturing ecosystems, where predictive maintenance and oil condition monitoring technologies will further optimize lubricant consumption and machine performance.

The Reasons Behind the Market’s Growth

Several industrial and technological factors are contributing to the steady expansion of the machine tool oils market worldwide.

Rapid Industrial Automation

The growing adoption of automated manufacturing systems and CNC machinery across industrial sectors is increasing the need for specialized lubrication products capable of supporting high-performance operations.

Expansion of Precision Manufacturing

Industries such as aerospace, automotive, electronics, and medical devices require highly accurate machining processes, increasing demand for advanced machine tool oils that ensure operational stability and component protection.

Rising Demand for Synthetic Lubricants

Manufacturers are increasingly preferring synthetic and semi-synthetic machine oils due to their superior thermal stability, extended oil life, and reduced maintenance requirements.

Workplace Safety and Environmental Regulations

Stringent regulations related to industrial emissions, mist exposure, and lubricant disposal are encouraging the adoption of environmentally friendly and low-mist lubricant formulations.

Growth in Emerging Manufacturing Economies

Countries such as China and India are witnessing rapid industrial expansion and growing machine tool installations, creating strong demand for machine tool lubrication systems.

Top Segment Analysis

Product Type Analysis

Hydraulic Oil Leads Market Demand

Hydraulic oil is expected to dominate the global machine tool oils market, accounting for nearly 45% of market share in 2026. These oils play a critical role in powering hydraulic systems responsible for clamping, positioning, and feeding operations in CNC lathes, milling machines, and industrial presses.

Application Analysis

Bearings Segment Maintains Strong Position

Bearings represent the leading application segment with approximately 20% market share, driven by the growing requirement for friction reduction, operational smoothness, and equipment durability across manufacturing facilities.

Country-Level Growth Analysis

- China: ~6.8% CAGR

- India: ~6.3% CAGR

- Germany: ~5.8% CAGR

- France: ~5.3% CAGR

- United Kingdom: ~4.8% CAGR

- United States: ~4.3% CAGR

China and India are emerging as the fastest-growing markets due to rapid industrialization, large installed machine tool bases, and increasing investments in manufacturing infrastructure.

Regional Development: Asia-Pacific Emerges as Manufacturing Hub

Asia-Pacific is expected to remain the dominant regional market for machine tool oils throughout the forecast period due to expanding industrial production and manufacturing modernization.

China

China continues to lead global machine tool oil consumption, supported by its massive metalworking and industrial manufacturing ecosystem.

India

India is witnessing rising adoption of advanced manufacturing systems across automotive, engineering, and electronics industries, strengthening lubricant demand.

Germany

Germany maintains strong demand due to its precision engineering industry and growing adoption of high-performance synthetic lubricants.

United States

The U.S. market is being driven by industrial maintenance requirements and modernization of manufacturing facilities.

Challenges, Trends, Opportunities, and Drivers

Drivers

- Rising industrial automation

- Increasing CNC machine adoption

- Expansion of metalworking industries

- Growth in precision manufacturing

Opportunities

- Development of bio-based lubricants

- AI-driven oil condition monitoring systems

- Long-life synthetic lubricant innovations

- Smart factory integration

Trends

- Shift toward low-mist lubricant formulations

- Adoption of predictive maintenance technologies

- Increasing use of synthetic and semi-synthetic oils

- Sustainability-focused lubricant development

Challenges

- Fluctuating crude oil prices

- Disposal and environmental compliance costs

- Competition from alternative lubrication technologies

- High costs of premium synthetic lubricants

Competitive Landscape

The machine tool oils market remains moderately competitive, with major companies focusing on advanced formulations, OEM approvals, and global distribution expansion.

Key companies operating in the market include:

- Exxon Mobil Corporation

- Lubriplate Lubricants Company

- Eastern Petroleum Private Limited

- Petro-Canada Lubricants

- Bel-Ray Company

These companies are increasingly investing in synthetic lubricant technologies, extended-life oil formulations, and environmentally sustainable solutions to strengthen their market positions.

Future Outlook: Smart Manufacturing to Shape the Next Decade

The future of the machine tool oils market will be closely linked with the evolution of advanced manufacturing technologies and smart industrial systems. As factories become more digitized and production efficiency becomes increasingly critical, machine tool oils will play an essential role in ensuring operational reliability and reducing equipment downtime.

The integration of predictive maintenance systems, AI-based lubricant monitoring, and sustainable lubrication technologies is expected to redefine industrial lubrication strategies over the coming decade. Manufacturers that invest in advanced formulations capable of meeting evolving industrial and environmental standards are likely to gain a strong competitive advantage.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website:

https://www.futuremarketinsights.com/reports/machine-tool-oils-market