\

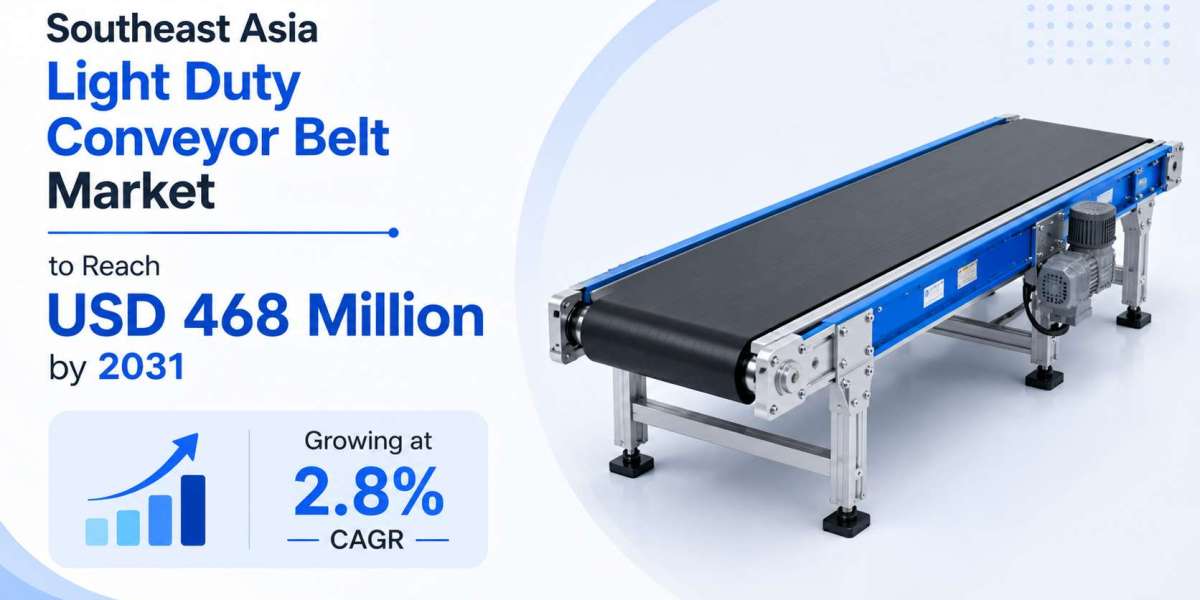

The Southeast Asia light duty conveyor belt market was valued at USD 387 million in 2023 and is projected to reach USD 468 million by 2031, exhibiting a CAGR of 2.8% during the forecast period.

Light duty conveyor belts are integral components in automated material‑handling systems, designed to transport lightweight goods and packages efficiently. They are characterized by moderate strength, flexibility and low power consumption, making them suitable for applications such as packaging, food processing, pharmaceuticals and e‑commerce fulfillment centers across countries like Singapore, Malaysia, Thailand and Indonesia.

***Download FREE Sample Report:***

Southeast Asia Light Duty Conveyor Belt Market - View in Detailed Research Report

The market is experiencing rapid growth due to several factors, including the explosive expansion of e‑commerce and logistics networks in the region, rising automation investments in manufacturing hubs such as Vietnam’s electronics sector, and increasing demand for energy‑efficient handling solutions. Moreover, regional players such as Habasit, Forbo‑Siegling and Intralox are accelerating product development focused on sustainable materials like thermoplastic elastomers (TPE) and IoT‑enabled sensors for predictive maintenance, further fueling adoption throughout Southeast Asia.

What is a Light Duty Conveyor Belt?

A light duty conveyor belt is a conveyor system component engineered to move light to medium‑weight products at moderate velocities while minimizing energy consumption and wear. These belts are fabricated from flexible, abrasion‑resistant materials such as coated PVC, TPU or composite fabrics and are preferred in high‑throughput environments where speed, reliability and hygiene are paramount. Their design allows rapid change‑over, low maintenance and easy integration with control systems, making them indispensable for modern fulfillment centers, e‑commerce warehouses and food‑grade processing lines.

“The flexibility and cost‑effectiveness of light duty belts make them an attractive solution for companies seeking to upgrade existing infrastructure or build new automated lines without incurring prohibitively high capital expenditures,” notes a senior analyst at Intel Market Research.

Key Market Drivers

1. Expanding E‑commerce Market in ASEAN

The unprecedented growth of online retail in Indonesia, Malaysia, Thailand, Vietnam and the Philippines has created a surge in parcel‑sorting centers and automated fulfillment hubs. Light duty belts provide the necessary speed and low power consumption required by these high‑volume environments, enabling operators to meet tight delivery timelines and customer expectations.

2. Accelerated Automation in Manufacturing Hubs

Southeast Asia has solidified its position as a global manufacturing corridor, particularly in Vietnam’s electronics, automotive and textile sectors. Enterprises in these industries are adopting automated material handling solutions to improve throughput, accuracy and safety, resulting in higher demand for belts that can handle a diverse range of product weights while maintaining reliability.

3. Focus on Energy Efficiency and Sustainability

Utilities costs and sustainability targets are influencing procurement decisions. Light duty belts crafted from low‑friction, thermoplastic materials reduce rolling resistance and energy consumption. In addition, many manufacturers in the region are transitioning to eco‑friendly polymers such as TPE, which offer comparable durability with a lower environmental footprint.

4. Government Incentives for Smart Manufacturing

ASEAN governments are investing in smart factory initiatives, digitalization, and Industry 4.0 readiness. Financial incentives, tax breaks and research grants are supporting the adoption of automated solutions, with belt integration being a critical component of these initiatives.

Market Challenges

Limited Technical Expertise

Many small‑to‑medium enterprises lack in‑house engineering teams capable of designing or customizing conveyor systems to meet specific throughput and product‑handling requirements. Dependence on generic belt solutions can lead to inefficiencies or reduced performance.

Supply Chain Volatility

Fluctuations in raw‑material prices (e.g., synthetic fibers, rubber compounds) and disruptions in global supply chains can affect lead times and cost stability for belt manufacturers and end users.

Regulatory Divergence Across ASEAN

While electric power availability and quality differ regionally, variations in safety and environmental regulations can complicate cross‑border procurement and implementation of conveyor systems.

Market Opportunities

Smart Belt Technologies

IoT‑enabled sensors and predictive‑maintenance analytics integrated into belts provide real‑time monitoring of tension, wear and temperature. These capabilities enable proactive maintenance, reduce downtime and extend belt life, offering a significant value proposition for manufacturers pursuing digital transformation.

Eco‑Friendly Belt Materials

The growing emphasis on sustainability has spurred demand for biodegradable or recyclable belts. Singapore, Indonesia and other markets where regulatory standards favor green materials are rapidly adopting these solutions, creating a premium segment for high‑quality, eco‑friendly belts.

Expansion of Free‑Trade Zones

New free‑trade zones and industrial parks are fostering concentrated manufacturing activity. These clusters provide a fertile ground for the rapid deployment of standardized conveyor infrastructures, enabling fast scaling for producers and logistics operators alike.

Market Segmentation

By Type

Coated PVC Belts

Thermoplastic Polyurethane (TPU) Belts

Composite Fabric Belts

By Application

Food Processing

E‑commerce Logistics

Pharmaceutical Packaging

Textile Manufacturing

Other Industrial Uses

By End User

Manufacturing Plants

Distribution Centers

Retail Outlets

Technology Hubs

By Region

Singapore

Malaysia

Thailand

Indonesia

Vietnam

Philippines

Competitive Landscape

The Southeast Asian market is anchored by a handful of globally active manufacturers that have built extensive sales and service networks across Indonesia, Malaysia, Thailand, Vietnam, Singapore and the Philippines. Habasit and Forbo‑Siegling continue to dominate the high‑end, hygienic belt niche, leveraging advanced PVC and TPU formulations that meet stringent food‑grade standards. Intralox, with its modular plastic belting technology, has captured a growing share of e‑commerce fulfillment centers that require rapid change‑over and low‑maintenance solutions. Regional champions such as PT. Garmo Pratiwi (Indonesia), GE Belt (Singapore) and Thailand’s Ryoh Machinery complement these leaders by offering cost‑effective, locally sourced products that satisfy the price sensitivity of small‑ and medium‑scale logistics operators. Collectively, these firms account for more than 45 % of the regional market volume, while the remainder is fragmented among specialized suppliers focusing on niche applications such as pharmaceutical packaging or textile processing.

Beyond the primary tier, a vibrant second layer of manufacturers competes on customization, rapid delivery and compliance with emerging sustainability guidelines. Companies such as Malaysia’s TUSCO, Vietnam’s Vina Belt, and the Philippines’ Unichrome Conveyor Systems have introduced belts with recycled‑content plastics and low‑noise designs to address environmental regulations and urban warehouse constraints. Chinese exporters like Shanghai YongLi Belting maintain a strong presence in bulk‑order projects, particularly within large‑scale distribution hubs. Emerging players including Indonesia’s PT. Mekanik Beltindo and Thailand’s Siam Belt Co. are gaining traction through aggressive investment in IoT‑enabled monitoring kits that support predictive maintenance, a feature increasingly demanded by Industry 4.0‑focused manufacturers.

List of Key Light Duty Conveyor Belt Companies Profiled

Habasit

Forbo‑Siegling

Intralox

GE Belt (Singapore)

PT. Garmo Pratiwi (Indonesia)

Ryoh Machinery (Thailand)

TUSCO (Malaysia)

Vina Belt (Vietnam)

Unichrome Conveyor Systems (Philippines)

Shanghai YongLi Belting Co., Ltd.

PT. Mekanik Beltindo (Indonesia)

Siam Belt Co. (Thailand)

Derco (Singapore)

Volta Belting Technology Ltd.

Esbelt (Vietnam)

Sector‑Specific Trends

**E‑commerce Logistics Expansion** – The rapid rise of online retail across Indonesia, Malaysia, Thailand, Vietnam and the Philippines is fueling a steady demand for light duty conveyor belts in parcel‑sorting and fulfillment centers. Warehouse operators are adopting belts with anti‑static coatings and easy‑clean surfaces to handle high‑volume, lightweight packages efficiently. This logistics surge is supported by government initiatives that improve last‑mile connectivity and by private investment in automated distribution hubs, creating a clear upward trend for conveyor belt installations throughout Southeast Asia.

**Material Advancements** – Manufacturers are increasingly offering belts constructed from thermoplastic elastomers (TPE) and enhanced PVC blends that combine durability with lower energy consumption. These materials provide better resistance to oil, grease and frequent cleaning cycles, which is essential for food‑processing and pharmaceutical facilities that are expanding in the region. The shift towards sustainable polymers also aligns with emerging environmental regulations in several Southeast Asian economies.

**Smart Belt Innovations** – IoT‑enabled sensors are being integrated into belt systems to enable predictive maintenance and real‑time performance monitoring. By collecting data on belt tension, temperature and wear, operators can schedule interventions before failures occur, reducing downtime in high‑throughput environments. This trend reflects the broader Industry 4.0 adoption in Southeast Asian manufacturing, where connectivity and data‑driven decision‑making are becoming standard practice.

Regional Analysis

**Indonesia** – Rapid industrialization, combined with a surge in e‑commerce fulfillment centers and food‑processing plants, is creating a persistent demand for efficient material‑handling solutions. Government incentives for manufacturing zones and the ongoing modernization of logistics networks are encouraging investments in automated conveyor systems. The rise of local belt manufacturers leveraging cost‑effective production capabilities enhances market accessibility for small and medium enterprises seeking scalable automation.

**Vietnam** – Vietnam’s emergence as a regional export hub has heightened the need for streamlined material handling in garment factories and electronics assembly lines. Smart‑warehouse initiatives, paired with expanding cold‑chain logistics for food products, compel manufacturers to integrate lightweight, hygienic belts. Trade agreements stimulating foreign direct investment further promote the development of high‑throughput distribution centers reliant on efficient conveyor solutions.

**Thailand** – Thailand is enhancing infrastructure through upgrades to inland ports, highway freight corridors and regional distribution hubs. These projects create opportunities for conveyor belt integration, especially in automated material‑handling cores near the Eastern Economic Corridor and at modernized seaports that aim to improve container throughput. Public‑private partnerships reinforce Thailand’s role as an ASEAN trade gateway, consequently driving belt demand.

**Malaysia** – Malaysia’s Industry 4.0 roadmap emphasizes IoT‑enabled equipment and energy‑efficient operations. Conveyor manufacturers are embedding sensors for predictive maintenance and adopting eco‑friendly polymer compounds. Collaborations between research institutes and belt producers accelerate the rollout of low‑noise, high‑durability belts suitable for smart factories, with government grants for green manufacturing further incentivizing the transition to recyclable materials.

FAQs

Frequently Asked Questions

What is the current market size of the Southeast Asia Light Duty Conveyor Belt Market?

The market was valued at USD 387 million in 2023 and is projected to reach USD 468 million by 2031, exhibiting a CAGR of 2.8% during the forecast period.Which key players operate in this market?

Major players include Habasit, Forbo‑Siegling, Intralox, GE Belt (Singapore), TUSCO (Malaysia), and Vina Belt (Vietnam).What are the primary growth drivers?

The primary drivers are the explosive e‑commerce expansion, logistics network development, automation investments in local manufacturing hubs, and an increasing demand for energy‑efficient handling solutions.Which region dominates the market?

Southeast Asia remains the fastest‑growing region for light duty conveyor belts, driven by regional e‑commerce and manufacturing expansion.What emerging trends are shaping the market?

Emerging trends include sustainable material development and integration of IoT‑enabled sensors for predictive maintenance.

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in biotechnology, pharmaceuticals and healthcare infrastructure. Our research capabilities include:

Real‑time competitive benchmarking

Global clinical trial pipeline monitoring

Country‑specific regulatory and pricing analysis

Over 500+ healthcare reports annually

Trusted by Fortune 500 companies, our insights empower decision‑makers to drive innovation with confidence.

? Website: https://www.intelmarketresearch.com

? Asia‑Pacific: +91 9169164321

? LinkedIn: Follow Us

**Get Full Report Here:**

Southeast Asia Light Duty Conveyor Belt Market - View Detailed Research Report