Market Overview and Growth Outlook

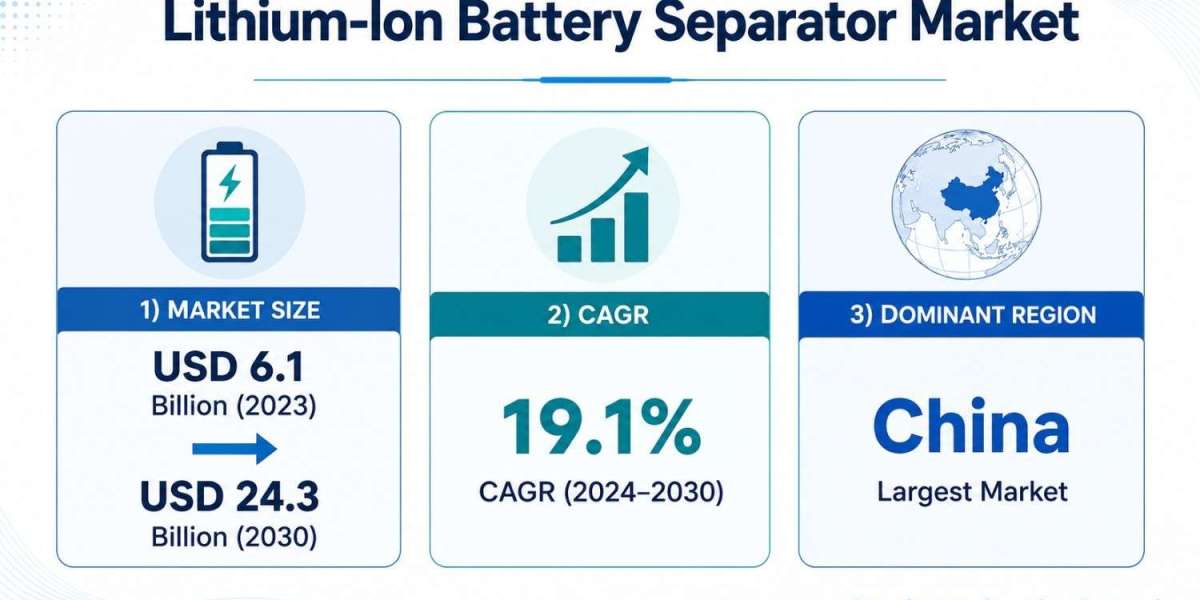

The industry outlook for lithium-ion battery separators is defined by rapid value creation and increasingly demanding product requirements. The Lithium-Ion Battery Separator Market was estimated at USD 6.1 billion in 2023 and is expected to reach USD 24.3 billion in 2030, expanding at a CAGR of 19.1% throughout the 2024–2030 forecast period.

“The Lithium-Ion Battery Separator Market is expected to grow at a CAGR of 19.1% during 2024–2030.” The separator’s role extends beyond physical electrode separation. It must permit ion flow, remain stable against electrolytes and electrode materials, resist battery operating temperatures, and prevent internal short circuits that could undermine performance, life, or safety.

The Lithium-Ion Battery Separator Market outlook reflects expanding battery demand and a shift toward higher-performance cells. Electric vehicles, renewable storage systems, industrial applications, and consumer electronics are increasing consumption, while battery innovation and safety regulation encourage separators with improved thickness control, porosity, adhesion, thermal characteristics, chemical stability, and manufacturing efficiency.

Request a free sample report:

https://www.stratviewresearch.com/Request-Sample/lithium-ion-battery-separator-market#form

Market Segmentation Analysis

Automotive, Industrial, and Consumer Electronics are the End-Use Industry Type categories. Automotive holds the largest share and should remain the biggest demand generator. Industrial is forecast to grow fastest. Electric vehicle production supports automotive volume, while industrial demand benefits from efficient energy storage, automated manufacturing, robotic systems, renewable integration, and sustainability-focused operations.

PE (UHMWPE and Others), PP, and Others are the Material Type categories. PE accounted for the largest market share and should remain the preferred material. Its material characteristics support separator porosity, strength, chemical compatibility, thermal performance, and electrical insulation. These properties are especially relevant as electric and hybrid vehicle batteries require greater energy density, power output, and safety.

Dry and Wet are the Medium Type categories. Wet separators are expected to remain largest and grow fastest. They are widely used for low-thickness applications and can support increased volumetric energy density. Their electrolyte-management and thermal characteristics are also well suited to batteries requiring higher energy density, faster charging, longer cycle life, and reliable high-power performance.

Films and Nonwovens are the Separator Type categories. Films hold the largest share and are expected to remain dominant. Nonwovens should register faster growth. Films offer controlled pores, uniformity, durability, and mature manufacturing processes. Nonwoven development focuses on higher porosity and tortuosity, characteristics that improve ionic conductivity and electrolyte retention within a lithium-ion battery cell.

Regional Market Insights

China will likely remain the largest market because of its extensive manufacturing capabilities for lithium-ion batteries and components. Numerous production facilities, economies of scale, efficient processes, and comparatively lower costs reinforce this position. Large electric vehicle, electronics, and energy-storage markets further increase battery output and demand for separators meeting manufacturers’ quality and cost requirements.

North America is expected to record the highest growth. The region is seeing a significant increase in electric vehicle adoption, alongside separator manufacturers opening production plants. This development expands regional manufacturing capacity while placing supply closer to battery demand, creating a structurally stronger North American role within the global separator market.

Emerging Trends Shaping the Lithium-Ion Battery Separator Market

Commercial development is moving toward advanced adhesion, controlled deposition and coating, low-temperature assembly, and semi-solid battery manufacturing technologies. These focus areas demonstrate the growing connection between separator materials and cell-production processes. Separator suppliers are increasingly addressing not only membrane properties but also electrode adhesion, coating behavior, assembly speed, interface stability, and compatibility with evolving battery architectures.

Material efficiency is developing alongside safety. New flame-retardant separator technology has demonstrated reductions of more than 40% in coating base weight versus alumina ceramic coatings and more than 20% in moisture content. The use of heat-absorbing materials that release flame-inhibiting gases shows how separator design can combine thermal protection, lighter coatings, and manufacturing-performance improvements.

Key Growth Drivers of the Market

- Larger automotive demand: Vehicle electrification requires substantial battery packs and creates high-volume separator consumption across individual lithium-ion cells.

- Broader energy storage use: Renewable power integration and efficient storage requirements expand industrial battery deployments and separator needs.

- Established electronics consumption: Lithium-ion batteries remain widely used in consumer electronics, maintaining demand for dependable separator materials.

- Continuous technology advancement: Cell designs requiring greater energy density and charging performance need separators with improved structures, interfaces, and thermal properties.

- Performance-cost optimization: Ongoing efforts to improve battery output and safety while reducing costs encourage material, coating, thickness, and manufacturing innovation.

Competitive Landscape

Top Companies in the Market

- SEMCORP Group

- Shenzhen Senior Technology Material Co., Ltd.

- Asahi Kasei Corporation

- Sinoma Science & Technology Co., Ltd.

- SK Innovation Co., Ltd.

- Toray Industries

- UBE Corporation

- ENTEK International

The global market is highly consolidated and includes fewer than 50 participants. Companies compete through price, service offerings, and regional presence. This competitive structure increases the strategic relevance of production scale, customer access, geographic manufacturing footprints, and the ability to deliver separator products that meet changing battery-performance and safety requirements.

Conclusion and Strategic Outlook

The Lithium-Ion Battery Separator Market outlook remains anchored in a projected 19.1% CAGR during 2024–2030 and a forecast value of USD 24.3 billion by 2030. Demand growth is associated with expanding battery volumes and progressively higher requirements for density, charging, cycle life, safety, cost, and manufacturing performance.

The segment structure points to Automotive, PE, Wet, and Films as continuing leaders. Industrial, Wet, and Nonwovens carry stated faster-growth positions in their relevant categories. China’s scale and North America’s growth provide distinct regional dynamics, while advanced coating, adhesion, flame resistance, and low-thickness technologies define the market’s developing strategic direction.

FAQs – Lithium-Ion Battery Separator Market

1. What is the current market size and 2030 outlook?

The Lithium-Ion Battery Separator Market was estimated at USD 6.1 billion in 2023. The market is expected to reach USD 24.3 billion by 2030.

2. What CAGR does the market outlook indicate?

The expected CAGR is 19.1% during 2024–2030. This expansion is associated with increasing lithium-ion battery adoption and separator-performance requirements.

3. What industries are driving separator demand?

Automotive, industrial, and consumer electronics applications generate separator demand. Electric vehicles, renewable energy storage, automation, battery development, and safety regulation are among the explicitly stated growth factors.

4. Where is regional demand concentrated?

China is forecast to remain the largest market due to battery manufacturing scale and demand from major battery-using sectors. North America is expected to grow fastest as EV adoption rises and manufacturers establish separator plants.

5. What is the strategic investment outlook?

The growth forecast indicates expanding commercial requirements, but market participants must meet demanding safety and performance standards. Competition among fewer than 50 global players also places importance on cost, service offerings, manufacturing capacity, and regional presence.